While for the owners of residential properties, a home loan’s equated monthly instalment (EMI) is something which they can’t control, they can still make use of maximum tax benefits that come from owning a house. Whether you’re planning to buy a residential property in Delhi NCR or want to sell your house, you can avail various tax exemptions and also save your capital gains tax by following some simple rules.

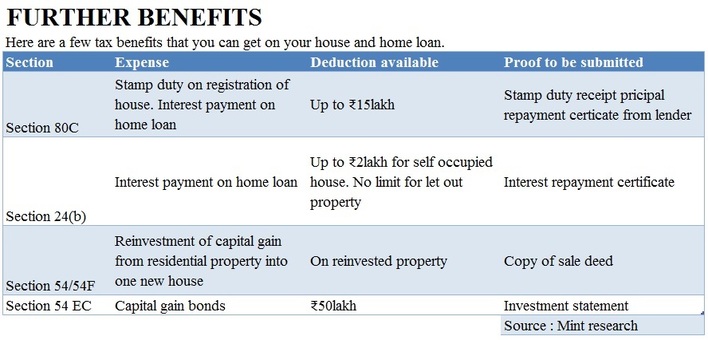

Whenever you buy a new house or residential property, you also incur several incidental charges like brokerage, stamp duty, registration fee and even the cost of shifting to a new place. While not all the expenses qualify for a tax deduction, there are few that can give you significant tax benefits. Few tax benefits that you can get on your house and home loan include the amount you pay as stamp duty for registration of your property. You can avail tax exemptions of up to Rupees 1.5 lakh on stamp duty under section 80C of the Income Tax (IT) Act, 1961. Stamp duty is charged by the state government as a percentage of fees on the property value. It varies from state to state and is lower for women in some states.

Besides stamp duty, one can also avail tax exemptions on home loan by breaking down EMI into two components: principal and interest. The amount paid as principal repayment qualifies for deduction of up to Rupees 1.5 lakh under section 80C, whereas interest portion qualifies for deduction under section 24(b) of the IT Act. If you’ve a self-occupied property, you can claim a deduction on the interest up to Rupees 2 lakh, and if the property is rented out, you can get rebate on entire interest due from this year onwards.

In case you’re planning to sell your house, you need to understand about capital gains tax that arises when you sold out your property at higher prices than on which you had bought. Capital gains tax is the tax on the profit you made by selling your house, and varies depending on the period of holding the property. Capital gains tax is of two types: short-term capital gains tax (STCG) and long-term capital gains tax (LTCG). While STCG applied on a property held for less than three years and taxed marginally, LTCG applied on residential properties held for three years or above and taxed at the whopping rate of 20 per cent with indexation.

You can save tax on your LTCG by investing the gains you made into another residential property within a period of one year before or two years after the date of transfer of the property. The procedure is mentioned under section 54/54F of the IT Act. Also, in case of an under-construction project, the property should be ready within three years from the date of transfer of the old property to avail tax exemptions. One more way to save tax on LTCG is by investing the gains into specified bonds under section 54EC of the Income Tax Act. The maximum limit to invest in capital gain bonds (specific bonds) is Rupees 50 lakh as per the new rules under Finance Act, 2014. The investment should be made within six months from the date of sale or before the filing of income-tax return, whichever is earlier.

Mr. Anil Mithas, Chairman & Managing Director at Unnati Fortune Group, says – “The rise in demand for residential properties in Delhi NCR gave way to several residential projects in Noida and other regions. Many people are looking to buy new residential properties and selling the existing ones. By taking into considerations these simple and smart steps, one can make use of several tax benefits that come from owning a house.”

Follow Mr. Anil Mithas on Twitter & Facebook

Whenever you buy a new house or residential property, you also incur several incidental charges like brokerage, stamp duty, registration fee and even the cost of shifting to a new place. While not all the expenses qualify for a tax deduction, there are few that can give you significant tax benefits. Few tax benefits that you can get on your house and home loan include the amount you pay as stamp duty for registration of your property. You can avail tax exemptions of up to Rupees 1.5 lakh on stamp duty under section 80C of the Income Tax (IT) Act, 1961. Stamp duty is charged by the state government as a percentage of fees on the property value. It varies from state to state and is lower for women in some states.

Besides stamp duty, one can also avail tax exemptions on home loan by breaking down EMI into two components: principal and interest. The amount paid as principal repayment qualifies for deduction of up to Rupees 1.5 lakh under section 80C, whereas interest portion qualifies for deduction under section 24(b) of the IT Act. If you’ve a self-occupied property, you can claim a deduction on the interest up to Rupees 2 lakh, and if the property is rented out, you can get rebate on entire interest due from this year onwards.

In case you’re planning to sell your house, you need to understand about capital gains tax that arises when you sold out your property at higher prices than on which you had bought. Capital gains tax is the tax on the profit you made by selling your house, and varies depending on the period of holding the property. Capital gains tax is of two types: short-term capital gains tax (STCG) and long-term capital gains tax (LTCG). While STCG applied on a property held for less than three years and taxed marginally, LTCG applied on residential properties held for three years or above and taxed at the whopping rate of 20 per cent with indexation.

You can save tax on your LTCG by investing the gains you made into another residential property within a period of one year before or two years after the date of transfer of the property. The procedure is mentioned under section 54/54F of the IT Act. Also, in case of an under-construction project, the property should be ready within three years from the date of transfer of the old property to avail tax exemptions. One more way to save tax on LTCG is by investing the gains into specified bonds under section 54EC of the Income Tax Act. The maximum limit to invest in capital gain bonds (specific bonds) is Rupees 50 lakh as per the new rules under Finance Act, 2014. The investment should be made within six months from the date of sale or before the filing of income-tax return, whichever is earlier.

Mr. Anil Mithas, Chairman & Managing Director at Unnati Fortune Group, says – “The rise in demand for residential properties in Delhi NCR gave way to several residential projects in Noida and other regions. Many people are looking to buy new residential properties and selling the existing ones. By taking into considerations these simple and smart steps, one can make use of several tax benefits that come from owning a house.”

Follow Mr. Anil Mithas on Twitter & Facebook

RSS Feed

RSS Feed